Investment trends are defined by a few significant events that become engraved in investors’ minds. These can be huge positive outcomes such as Facebook’s acquisition of WhatsApp for $22B, Twitter’s post IPO surge to $40B market cap, or Emergence Capital 300-fold return on a $4M investment in Veeva System. Such positive events generate momentum for the entire industry as they influence venture capitalists’ decisions. Although investors understand that there is a slim chance for a startup to become the next WhatsApp, Twitter or Veeva, it is just natural to be drawn to such examples when evaluating the potential outcome of an investment.

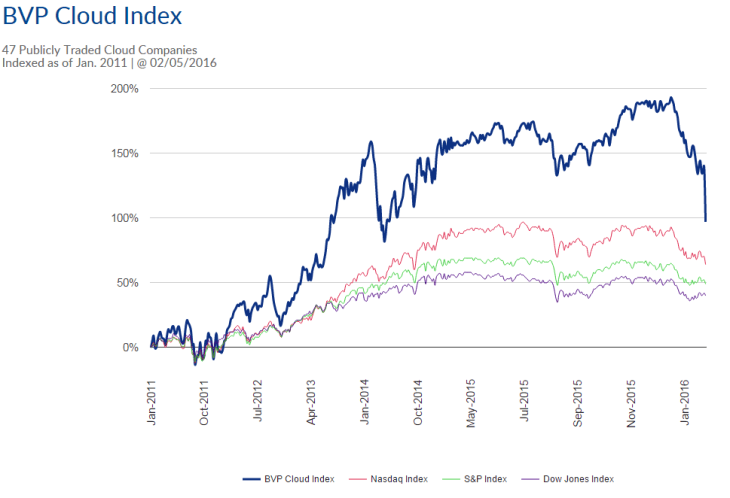

The same is true for large negative signals. Such signals can have a devastating effect on VC’s appetites to take on risk as investors contemplate gloomy scenarios. LinkedIn’s public valuation crash last Friday was one of these defining moments. The company lost 40% of its value in one trading day after providing a weaker than expected guidance for 2016 (despite the fact that it beat Q4 estimates). It was not only LinkedIn that crashed last Friday, but many other high-quality enterprise SaaS companies such as Tableau Software (down 40%), New Relic (down 23%), HubSpot and Zendesk (down 20% each). The chart below shows how BVP’s Cloud Index looked like on Friday:

LinkedIn’s stock crash is significant not only because of the extensive valuation drop, but also because it is difficult to find a satisfactory explanation for such a large downgrade by so many brokerages. Yes, lowering the guidance for 2016 should be reflected in the stock price. However, nothing substantial has really changed. LinkedIn still enjoys the same underlying network effect and core business, and it is impossible to see how it can be replaced as the dominant professional network in the next 5-10 years. Analysts’ explanations for the significant downgrade were a blurb of excuses, such as macroeconomic weakness (as if it wasn’t known before), reliance on enterprise subscription revenue instead of ad revenue (which is a more predictable and high-quality revenue source), or a plain “we were just wrong.” Goldman Sachs even went as far as calling LinkedIn “one of the most valuable assets on the Internet” while slashing the firm’s target price. What this really means is that Wall Street has just set a new norm for how it values high-growth SaaS companies. It might take some time until these companies will start enjoying the premium multiples they have grown accustomed to in recent years.

There is no doubt LinkedIn will be major discussion point in many investor meetings this week. VCs will reassess how they value deals, and what this means for their portfolio companies. LinkedIn was always viewed as the poster child for a strong internet company which benefits from a sustainable network effect and is able to monetize through a predictable subscription revenue. If it is valued at $12B enterprise value (4x revenue), then what does it mean for much smaller and riskier startups?

The median revenue multiple in BVP’s Cloud Index, which tracks 47 publicly traded Cloud companies, is down to 3.7x. Up until recently, VCs often valued high-growth SaaS startups at more than 15x the annual revenue run rate. This means that only after revenue has grown 4x (!), will investors overcome the multiple compression between the public and private markets, and start benefiting from the revenue growth. To further illustrate this point, if a VC valued a $15M revenue run-rate company at 15x run rate ($225M pre-money), and the company succeeds to grow revenue 8-fold (to $120M) and goes public, that company will most likely be valued at ~$450M by Wall Street, which is less than a 2x return for the investor.

Unless the public market quickly corrects back up, private investors will need to correct down to eliminate the wide valuation gap between the private and the public market. LinkedIn’s stock crash will likely expedite this process.