Now that we’ve talked about why SaaS is a beautiful business model, I’d like to give some guidance and tips to help do it right. Of course there is no “one size fits all” answer to how to do SaaS, but there are many things which are common across companies and many things we see that seem to work.

When you look at how the public market values SaaS companies today there is a very strong correlation to a few selected metrics. These are (some) of the metrics you will be valued on.

Growth

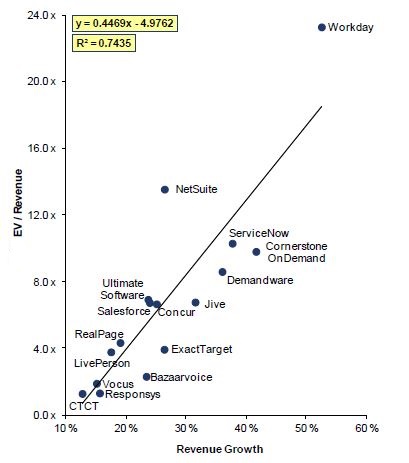

Growth is by far the most important metric of all. The annual growth rate will determine whether a startup is inscribed in the book of life or not. As a VC it is easier to pay a large premium for fast growing SaaS companies since you know the company will “grow” into the valuation, so you are basically just paying in advance. On the other hand, if a startup is not growing fast enough, it will find it very difficult to raise outside capital. Public investors are also willing to pay a large premium for fast growing companies especially in a low growth environment as we have today. The graph below shows the strong correlation between a SaaS company growth rate and the revenue multiple it gets in the public market:

source: Goldman Sachs

source: Goldman Sachs

Of course, growth at later stages is much more difficult and therefore more valuable. Achieving 10% incremental growth rate will result in a large increase in the revenue multiple a public company gets, but will have a limited impact on an early stage company valuation.

Retention

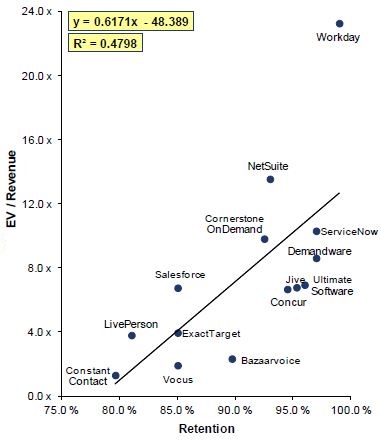

A lot has been written about the importance of gross and net retention for SaaS companies. I will elaborate on the importance of gross and net retention more in a separate post since many companies we meet still don’t pay enough attention to it. It is the #2 and arguably even the #1 most important metric for a SaaS company. As expected, both private and public investors care dearly about retention as can be seen by the strong correlation between retention and revenue multiples for public companies:

source: Goldman Sachs

source: Goldman Sachs

Gross Margins (GM)

This is where things start to become more tricky. As you can see below, public markets give very little importance to gross margins when they determine valuations. I like to segment the world into “high margin software companies” for anything north of 70-80% GM, “services companies” or “arbitrage games” (adtech companies typically fall into this bucket) for companies below 40-50% GM, and many of the in between fall in the “tech enabled companies”. Here is the public market view that shows very low correlation between GM and revenue multiple:

source: Goldman Sachs

source: Goldman Sachs

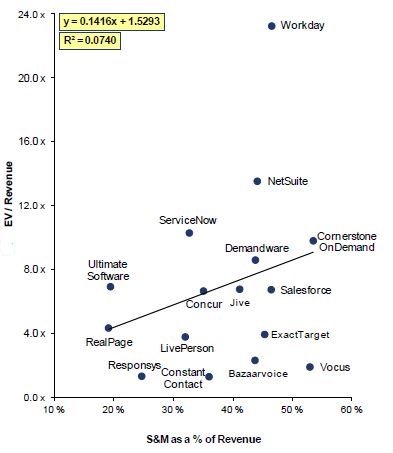

Sales and Marketing (S&M) spend

As discussed in the previous post, the nature of recurring revenue means you spend now to acquire a customer but get the benefit over a longer period of time. This is why public markets tend to care less about S&M spend as indicated in the graph below. We, on the other hand, view S&M spend as the throttle that lets you run your company’s engine: If churn is low, and your Go To Market (GTM) is efficient (as measured by your CAC ratio) then you want to further increase S&M spend. However, if you still haven’t found an efficient sales model or the right product / market fit then you want to throttle down S&M spend.

It is clear that the public market pays for growth drivers (revenue and retention) and cares much less about the rest. I think it’s an indicator of the frothiness of the market which doesn’t always value the viability of the underlining business model since it is more difficult to measure (this could also be a good opportunity for a long / short hedge fund on public SaaS companies). When we value a SaaS startup we try to assess things like CAC payback, long term gross margins and S&M effectiveness to determine the quality of the underlying model. I will touch on some of these things in the next blog post.

3 thoughts on “Grow or die”